Glassnode Launches IBIT Options Metrics, Advancing Bitcoin Analysis

Glassnode has introduced its IBIT options metrics suite, providing a new lens into how institutional markets are pricing Bitcoin ($BTC) risk and volatility. These tools mark a major step in analyzing the iShares Bitcoin Trust ETF (IBIT), the largest U.S.-listed spot Bitcoin ETF with over $61.1 billion in assets as of April 2026.

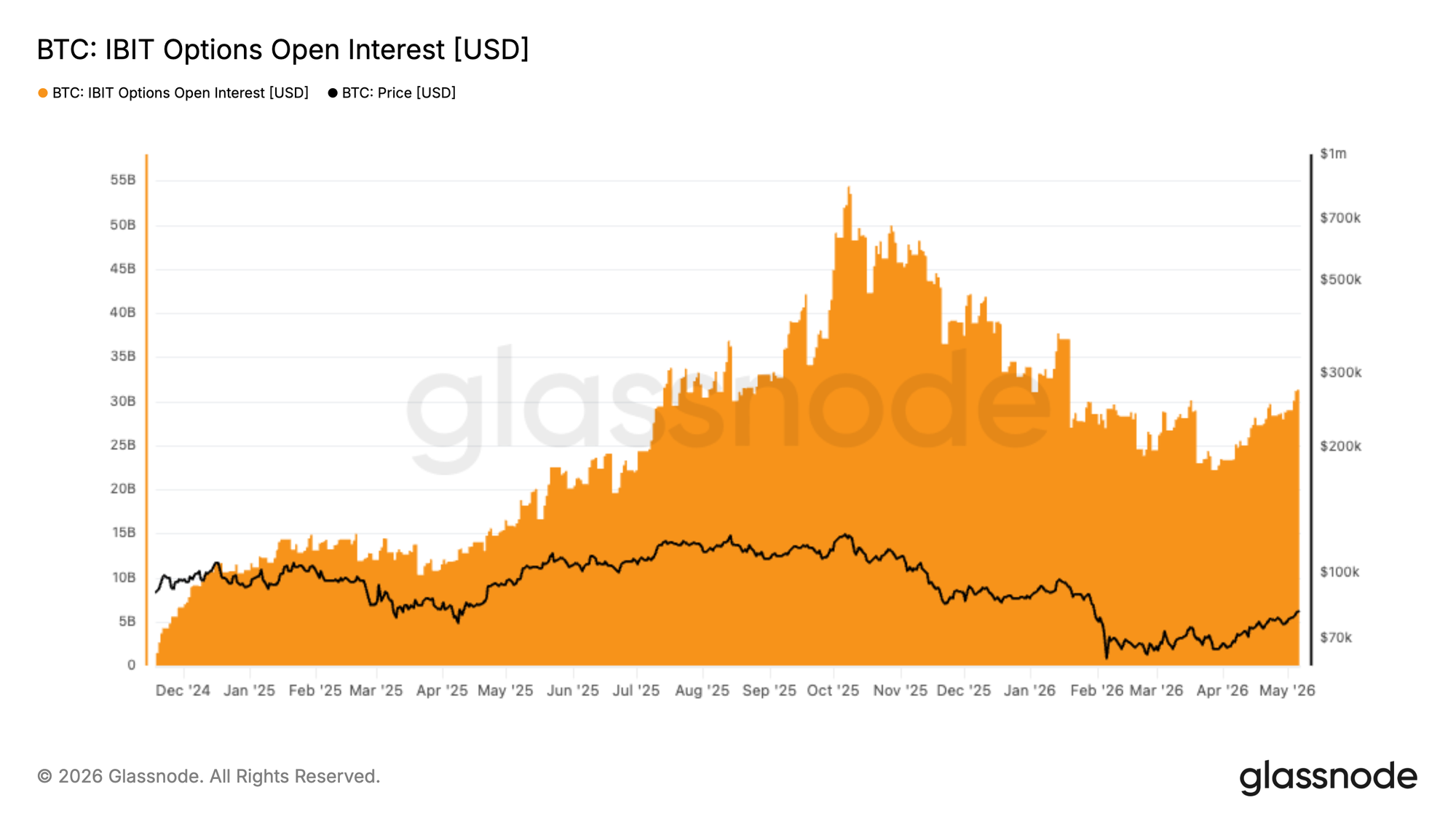

Options data is critical for institutional investors who rely on hedging, volatility trading, and risk management strategies. With the IBIT options market growing rapidly—open interest recently hit $27.6 billion, surpassing crypto-native Deribit's $26.9 billion—Glassnode's tools are tailored to track this increasingly important segment of Bitcoin's financial ecosystem.

Why IBIT Options Matter

Since the launch of spot Bitcoin ETFs in 2024, Bitcoin has moved deeper into traditional finance. IBIT options, first traded in late 2024, extend this trend by offering institutions a regulated way to manage Bitcoin exposure. These options function like equity ETF options, enabling users to hedge, speculate, and trade volatility without direct crypto custody.

Options markets also reveal more nuanced investor sentiment than spot or futures markets. They reflect how participants price upside, downside, and tail risk across time horizons. The ability to compare data from IBIT and Deribit options markets adds further value, highlighting divergences between traditional finance and crypto-native risk pricing. For example, as of May 5, IBIT options were more put-skewed than Deribit, suggesting ETF-linked investors are more focused on downside protection.

Glassnode’s Metrics: A Detailed Breakdown

Glassnode’s IBIT options suite includes over 40 metrics designed for institutional-grade analysis. Key metrics include:

- Open Interest: Total OI across all IBIT options, a key gauge of institutional engagement.

- Volume and Put/Call Ratios: Indicators of market sentiment and hedging activity.

- Implied Volatility (IV): Tracks ATM and delta-specific IV, helping investors monitor risk premiums across tenors.

- Skew Metrics: Measures asymmetry in volatility pricing, revealing market bias toward calls or puts.

Notably, Glassnode's skew analytics and implied volatility heatmaps provide a granular view of risk pricing. For example, normalized 25-delta skew data shows how ETF investors prioritize downside protection compared to crypto-native traders, offering actionable insights for analysts and traders.

Institutional Adoption and Market Impact

The rapid growth of IBIT options reflects Bitcoin's institutionalization. With $134.6 million in IBIT inflows reported in a single week during May, ETF-linked options activity is increasingly influencing Bitcoin price discovery. Market makers hedging options flows through IBIT shares can indirectly impact spot Bitcoin demand, further integrating traditional finance with crypto markets.

By offering a regulated, U.S.-listed alternative to offshore venues like Deribit, IBIT options are expanding Bitcoin's appeal among hedge funds, advisors, and structured-product desks. As Glassnode's tools gain adoption, they could reshape how institutional players analyze and engage with Bitcoin markets.

Looking Ahead

With Bitcoin trading at $79,222 as of May 14, 2026, IBIT options will likely play an even larger role in volatility and sentiment analysis. Glassnode’s metrics provide a real-time window into this evolution, enabling professionals to track shifts in institutional positioning and risk pricing. As IBIT and similar instruments continue to grow, they may redefine Bitcoin’s role in broader financial markets.